Reframe: planning as an investment

If you have been following this for a while, you might have noticed the pattern: I have a tendency of “thinking out loud” with my posts (i.e., it’s not by chance that I call the sort of free-willing audio version as such), so they often are representing stuff I am thinking and/or going through. And then no surprise either that sometimes posts will come in waves, building on each other.

That’s precisely the situation I am in right now. So it’s time to bring together two recent themes: the last post on reframing with the one from a few weeks ago on inverting to simplify the value problem.

The insight came up the other day as I was discussing with someone in my team about how to approach the upcoming planning session. As a great PM he is, he has done all the necessary due diligence, including so-called refinement sessions to figure out what options to consider and how they could look like.

The concept of planning as investment (or more in general, that to a large extent all we do in work is about “making bets”) has been on my mind, and by and large inspired the piece of simplifying by inverting the value problem.

But it was then (in the conversation with a PM from my team) when it fully hit me – what are the implications and the potential divergence depending on the lens you would use?

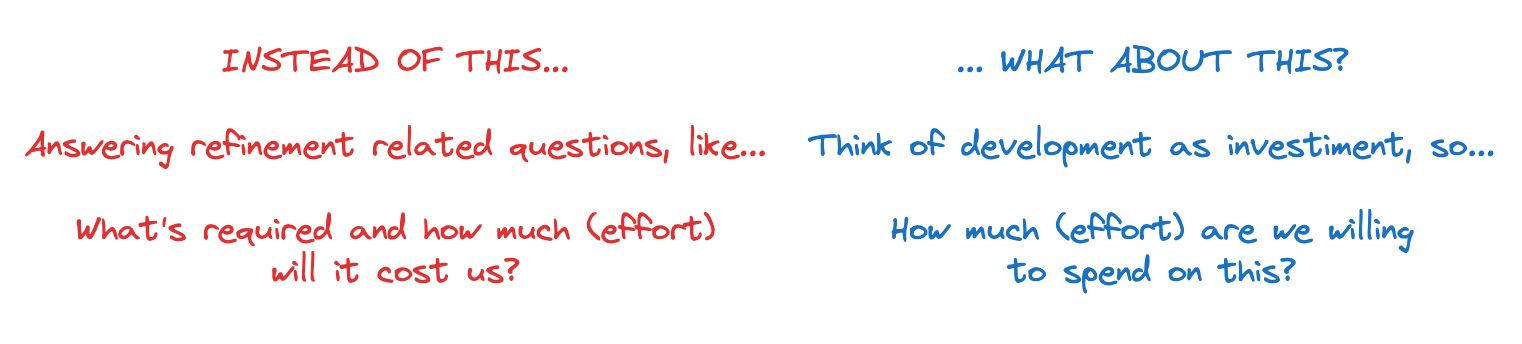

Because this is how a typical, let’s say, refinement-based planning approach tend to look like:

You figure out options you could consider.

You work them out until a level of detail to have both sufficient confidence on potential value as well as sufficient clarity on what we could potentially build (there’s an implied aspect of keeping the scope in check, but I’d argue not as deliberately as the alternative I will present next).

You somehow "put a finger on" sizing the efforts you’d need to put in (that’s largely what so-called refinement sessions are about).

Put in other words, the frame that tends to be taken is one that is “supply-side driven” – (as opposed to focusing on demand-side) – we take it from the perspective of what we can build. And we know that we humans tend to be overly optimistic and therefore risk investing and building more than we should...

So what’s the alternative, then!? Well, that’s precisely where the idea of “planning as investment” makes an entrance… What if we approach things from a different angle? What if we took the perspective of what’s our “level of ambition” to take a stab at solving a problem (or making enough progress related to something that matters to us)?

It might sound somewhat nuanced, but I believe the reframe makes a difference. I’m not even claiming it’s one or the other, I’m just suggesting taking another angle might cater for interesting conversation.

In principle it doesn’t matter so much the order you do – do you use the “planning as investment” frame as a mirror for what you figured out with refinement, or use the former to help constraining the latter. The second option looks more efficient, which brings me to how I’d personally do it.

Planning as investment – from idea to practice

Think about it this way – in figuring out what we could work on and realistically deliver in a time frame, what would the “poker chips” we would be using to bet (or invest)?

The simplest and arguably even more effective way is to consider the throughput that a team is capable of doing. But since we should accept the randomness aspect of delivering software (the real underlying reason why we consider adding elements for complexity of tasks like when we do story-pointing), we can’t just blindly use a data point to make projections against.

There’s a statistical sound technique that’s good to help dealing with randomness, it’s called Monte Carlo simulations. The underlying principle is simple:

If we simulate something too many times, a probabilistic pattern will emerge and we will be able to have higher confidence that we can forecast and talk about it confidently in turn (see what I did there?)

Here’s how I practically do it these days (with an example):

Extract a team’s sample (e.g., last 60 days) of daily recent story / task throughput

Aggregate weekly throughput scenarios

Simulate 1000x to build probabilistic pattern

Statistical patterns: how many throughput per week at least (or more)

P98 = 1 (equivalent to say that’s almost certain to happen as a scenario)

P85 = 3 (equivalent to 6 out of 7 times, i.e. a very high confidence scenario)

P75 = 4 (equivalent to 3 out of 4 times, i.e. a high confidence scenario)

P50 = 7 (equivalent to 1 out of 2 times, i.e. a typical, “flip of a coin”, confidence scenario)

Next up, I would use a few different confidence levels (e.g., P50, P75, P85) as possible scenarios of what I could plan against.

Am I willing to take quite some risks and be in a kind of “flip of a coin” situation, then P50 might be the way to go. Do I need to be super careful because I expect a lot of uncertainty along the way, or I need to set expectations with a high degree of reliability, then I might be using something like a P85.

Or just pick a number anywhere in between that seems to make sense (obviously while reflecting on the implications in terms of risk-taking). And whatever that is, it becomes an anchor for what we can plan against as a kind of overall (throughput) “budget”.

That’s the moment to trickle things down. Depending on how many options I am willing to consider to bet (or invest) on in a given time frame, I can now think about how I’d distribute that “budget” – in other words, what’s the sweet spot of the “level of ambition” of an option being considered balanced with hedging my risks by not putting all the “eggs in a single basket”, as the saying goes…

That’s roughly the “script”, and hopefully that is an inspiration in a small way to you. As it typically happens with things like these, it’s not about following a formula though, that’s just to help and frame the discussion. The real value is on the meaningful conversations that should emerge. And the fact that you’re doing it much more deliberately, in this case meaning that you’re using that (additional) lens of “planning as investment” as a way to better cater for a “demand-side” way of thinking about it.

By Rodrigo Sperb, feel free to connect, I'm happy to engage and interact. If I can be of further utility to you or your organization in getting better at working with product development, I am available for part-time advisory, consulting or contract-based engagements.

I like the idea of planning as investment, and have been writing about it for a while myself.

I liked how you introduced the idea of "planning" as "making a bet". That's useful for my own thinking.

But what I don't understand is the use of Monte Carlo.

Assuming you define how much you are willing to invest into something (the bet), then the Monte Carlo does add much value anymore. Or am I missing something in your argument?